CLASSICAL Economics

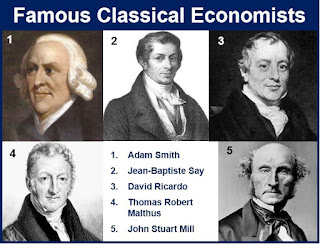

Classical Economics (Traditional financial aspects) is broadly viewed as the main current school of monetary idea. The expression "old style" alludes to work done by a gathering of market analysts in the eighteenth and nineteenth hundreds of years. Its significant engineers incorporate Adam Smith, David Ricardo, Thomas Malthus and John Stuart Plant.

A lot of their work was creating hypotheses about the manner in which markets and market economies work. Coming when Mercantilism held influence, accentuating the boosting of products and limiting imports, old style financial experts advanced a profoundly unique methodology. They basically viewed the economy as ready to keep up with its own balance through market influences, and that administration mediation as fake duties or different obstructions that upset the free progression of labor and products were hurtful to the economy.

Old style financial aspects ( Classical Economics) was a significant scholarly accomplishment. While new procedures of investigation were needed to resolve new inquiries, leading to the numerical definitions of the neoclassicals and others, and advances in innovation and changes in friendly mindfulness seem to have changed the financial scene, financial hypothesis today actually rests in numerous spaces, money related and exchange hypothesis to name however two, upon the establishments laid by traditional market analysts.

Classical economics refers to the school of economic thought that arose in Great Britain in the latter part of the eighteenth century. In the year 1776, David Hume died while Jacques Turgot and Marquis de Condorcet left their government posts. In that same year, though, the intellectual revolution they had contributed to, the Enlightenment, began to bear its principal fruit. It was a year of grand treatises. Adam Smith published his Wealth of Nations, the Abbé de Condillac his Commerce et le Gouvernement, Jeremy Bentham his Fragments on Government, and Tom Paine his Common Sense.

It was Smith's work that has been seen as laying the foundation of economics as a separate academic discipline. The central messages of his Wealth of Nations (1776) were laissez-faire—the virtues of specialization, free trade and competition, and so forth. Smith's vision of a free market economy, based on secure property, capital accumulation, widening markets, and a division of labor contrasted with the mercantilist tendency to attempt to "regulate all evil human actions" (Smith 1776).

Essentially this approach places total reliance on markets, and anything that prevent markets clearing properly should be done away with. The earlier belief that agriculture was the chief determinant of economic health was also rejected in favor of the development of manufacturing, and the importance of labor productivity was stressed. The theories put forward by the classical economists still influence economics to this day.

The classical economists strongly believed that the government should not intervene to try to correct this as it would only make things worse and so the only way to encourage growth was to allow free trade and free markets. Much of Adam Smith's early work was on this theme, and he introduced the notion of an "invisible hand" that guided economic activity and led to the optimum equilibrium.

Following Smith, in the struggle for succession as the voice of economic theorizing, three names emerged as strong contenders:

Jean-Baptiste Say,

Robert Malthus, and

David Ricardo.

These three had very different visions. Say (1803) wanted to take economic thought back towards the French-Italian demand-and-supply tradition. Malthus (1798, 1820) wanted to add a whole new emphasis, away from the obsessive intricacies of "value" and towards a more macroeconomic (and "dynamic") perspective. As Smith's laissez-faire approach, including specialization, free trade, and so forth, did not anticipate the magnitude of the economic and social upheavals that the industrial era was about to unleash, a new version, corrected, extended, and updated, was clearly needed. Ricardo (1817) wanted to do Smith all over again, but to do it properly this time.

Hence, out of these three, David Ricardo turned out to be the most successful and influential. With his 1817 treatise, Ricardo took economics to an unprecedented degree of theoretical sophistication. Ricardo's theory, the most clearly and consistently formalized of them all, became the "Classical system."

Coming at the end of the classical tradition, John Stuart Mill parted company with the earlier classical economists on the inevitability of the distribution of income produced by the market system. Mill pointed to a distinct difference between the market's two roles: allocation of resources and distribution of income. The market might be efficient in allocating resources but not in distributing income, he wrote, making it necessary for society to intervene

Adam smith father of classical Economics see below article

https://www.iemsnet.com/2020/01/adam-smith-father-of-economics-ugc-net.html

The Classical Theory

The fundamental principle of the classical theory is that the economy is self‐regulating. Classical economists maintain that the economy is always capable of achieving the natural level of real GDP or output, which is the level of real GDP that is obtained when the economy's resources are fully employed. While circumstances arise from time to time that cause the economy to fall below or to exceed the natural level of real GDP, self‐adjustment mechanisms exist within the market system that work to bring the economy back to the natural level of real GDP. The classical doctrine—that the economy is always at or near the natural level of real GDP—is based on two firmly held beliefs: Say's Law and the belief that prices, wages, and interest rates are flexible.

Say's Law. Supply create its own demand

According to Say's Law, when an economy produces a certain level of real GDP, it also generates the income needed to purchase that level of real GDP. In other words, the economy is always capable of demanding all of the output that its workers and firms choose to produce. Hence, the economy is always capable of achieving the natural level of real GDP.

The achievement of the natural level of real GDP is not as simple as Say's Law would seem to suggest. While it is true that the income obtained from producing a certain level of real GDP must be sufficient to purchase that level of real GDP, there is no guarantee that all of this income will be spent. Some of this income will be saved. Income that is saved is not used to purchase consumption goods and services, implying that the demand for these goods and services will be less than the supply. If aggregate demand falls below aggregate supply due to aggregate saving, suppliers will cut back on their production and reduce the number of resources that they employ. When employment of the economy's resources falls below the full employment level, the equilibrium level of real GDP also falls below its natural level. Consequently, the economy may not achieve the natural level of real GDP if there is aggregate saving. The classical theorists' response is that the funds from aggregate saving are eventually borrowed and turned into investment expenditures, which are a component of real GDP. Hence, aggregate saving need not lead to a reduction in real GDP

They also believe that interest rate prices and prices will remain fexible and change accordingly

Has anyone had experience with this and what would you recommend?

ReplyDeleteMy ex-husband and I got married online in 2020

I was told that I must file for divorce in my home state BUT I must be physically present (I am overseas). Can I use this https://onlinedivorcer.co.uk/online-divorce-northern-ireland?

Difficult situation I guess? No one I've talked to in my home state has any idea how to move forward with this...and I wish this nightmare was over.